Business taxes can be a nightmare for a lot of companies; especially small businesses that are trying to stay afloat. Things can get even tougher when it comes time to file your return and you end up on the wrong side of the ledger. So what should you do if you end up owing more business taxes than can afford?

First, don’t panic. There are steps you can take to get through the process. Then, make sure you still file your taxes on time, even if you know you don’t have the money. By delaying your filing you will be penalized further and owe even more money. So, file on time. If you’re already late, file as soon as possible.

If you can’t pay your debt in full at tax time, you do have some options. You can still make full payments a little late by filing for an extension. If you will have the funds shortly then this is a good option. Keep in mind, though, that you will be charged interest until the full amount is paid off.

You can also agree to the installment method, which allows you to make monthly payments until you pay off the debt in full. This requires a one-time set-up fee but it also allows you to choose the terms and the method of payment. You can also go with the offer in compromise route, which could lower your total bill if the IRS accepts your offer. Lastly, you could request that the IRS delay its collection if you absolutely don’t have the means to pay off your debt. This is called a temporarily delay collection.

Whatever method you choose, it’s always best to pay off whatever you can as soon as you can, and thus avoid further interest and penalties. If you find yourself in this situation, contact GROCO. We’ll help you determine which route is best for you. Call 1-877-CPA-2006, or click here.

If you have a bad credit rating, getting a home loan could prove difficult. There are however some steps you can take to give yourself the best chance of being approved.

1. Apply with a mortgage lender who does not use credit scoring

The majority of lenders use a computer-based system called credit scoring to assess your home loan application, says Kim Wight, a Personal Mortgage Adviser with Smartline.

"This means that the data collected in your application is given a rating or score and if the computer scores you as a bad risk, the application is declined before a real person has a chance to look at the application or hear your story as to why you have had credit problems in the past. In other words, 'computer says no'," she explains.

"By applying with a lender who does not use credit scoring, your application – and the reason for your past credit problems – will be assessed by a real person, who can evaluate your personal situation past and present and use this information to make their decision on your application; it can be a case of, 'human says yes'."

2. Avoid lenders mortgage insurance (LMI)

When you apply for a home loan, there are two approvals that have to be sought out if you borrow more than 80% of the value of the property. One is from the lender, and the other is from the mortgage insurer, who protects the lender in case you default on the loan.

"By having funds to cover 20% deposit, and other costs such as stamp duty and legal fees, you avoid having your application be assessed by the mortgage insurer, and you have a greater chance of the loan being approved," Wight says.

3. Demonstrate that you have improved your financial situation

"If you have had problems in the past, you need to show that you are now back on track by ensuring all current financial commitments are being paid on time," Wight says.

"This includes not only your loans and credit cards but your rent and utilities as well. Evidence of regular savings will also strengthen your application."

4. Apply to a specialist lender

Depending upon the severity your bad credit history, the mainstream lenders may not be able to assist you – but there are specialist lenders in the market place who price their products based on the element of risk.

"The interest rate is usually higher," Wight admits,"but people usually only stay in these products long enough for their credit situation to improve, and then they refinance to a lower rate."

5. Seek professional advice regarding your credit report

"There are a number of specialist credit repair agencies that may be able to assist you with cleaning up your credit report. It is advisable to speak with them or a solicitor to investigate if it is possible for adverse entries on your report to be removed," Wight says.

6. Shop around – but only in principle

It is important that you don't apply with lots of lenders as you shop around for a home loan, as each time you make an application, it is recorded against on your credit report."If lender after lender is declining your application, this will further impact your credit report," Wight says.

"At the outset, a mortgage broker can assess which lender is most likely to approve your loan application and what interest rate and charges may be applicable. It is important that you tell your broker the complete and honest story of why you have experienced credit problems so they can address the problems with the credit department of the lender."

In 2019, an estimated 28.3 million customers across four major insurers—GEICO, Progressive, State Farm and Allstate—are planning to switch insurance companies. These individuals represent a massive opportunity for challenger insurance brands to acquire new policy holders, provided they’re able to connect in a meaningful way with these individuals during their vital time of decision-making.

So how do you connect with today’s insurance switchers? Well, you start with an understanding of the individuals you intend to engage. As discussed in this recent post, part of this understanding should include why a given insurance companies’ customers are most likely to be switching. But it goes even deeper than that. To hone your messaging, you need insights into their motivations, their values and even their day-to-day activities and hobbies.

That’s where Resonate comes in. Our real-time consumer intelligence platform gives you access to the largest proprietary understanding of U.S. consumers’ habits, preferences, purchase drivers and more. For example, when you look across the customers currently seeking to replace their existing GEICO, Progressive, State Farm or Allstate policies, you find distinct differences in their preferred forms of entertainment—differences that can inform the messaging and cross-promotions that a company employs when trying to reach these groups. For example:

Both GEICO and Progressive switchers (audiences of 8.3 million and 4.2. million consumers, respectively) cite going to the movies and enjoying music as their top two forms of entertainment.

State Farm switchers (a population of 9.2 million consumers), on the other hand, are more likely to cite apparel shopping as their preferred form of entertainment.

Meanwhile, Allstate shoppers (6.6 million consumers) are most likely to cite art and photography as their preferred methods of entertainment.

With these distinctions in mind, insurance marketers would be well-served to target GEICO and Progressive switchers via messaging and partnerships that tap into their love of movies and music, while State Farm switchers are more likely to connect with messaging and promotions that tie into their love of fashion and shopping. Meanwhile, messages and promotions tied to a love of photography and the arts are most likely to resonate with Allstate switchers.

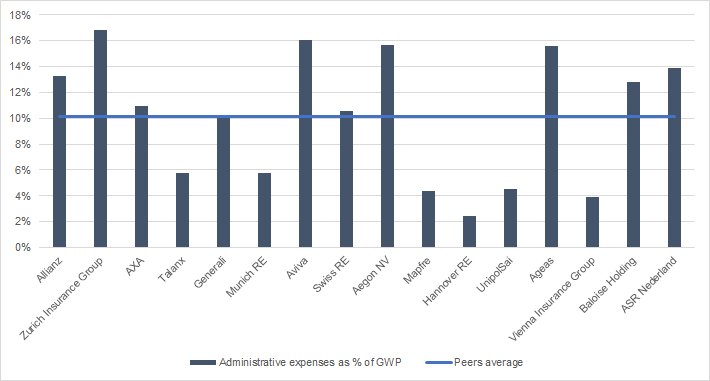

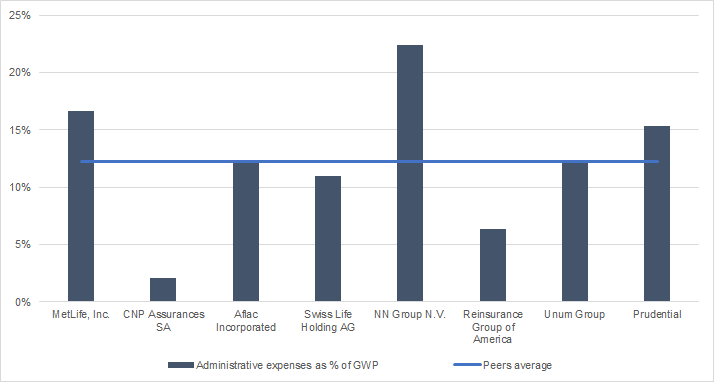

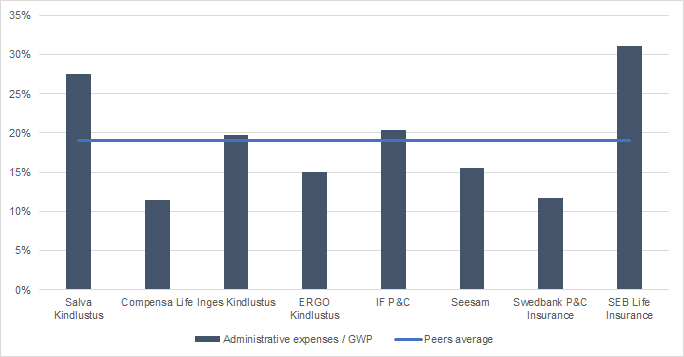

In this article we will provide you with data on the listed insurance companies across the world. We will show that the costs that occur for standard insurance companies that Black would almost eliminate, are quite significant. We have gathered financial data from various international and Estonian insurance companies between 2013 and 2016. The data shows that administrative expenses are quite high in the industry, thus there is a lot of cost cutting possible. It also becomes clear that smaller insurance companies would be first to fall, as their administrative expenses are relatively high to their gross written premiums.

Insurance companies have costs for admin expenses and net profit of Gross Written Premium. The industry average is 20%.

This is calculated by taking the average sum of the admin and net profit margins data of insurance companies provided below.

Administrative expenses

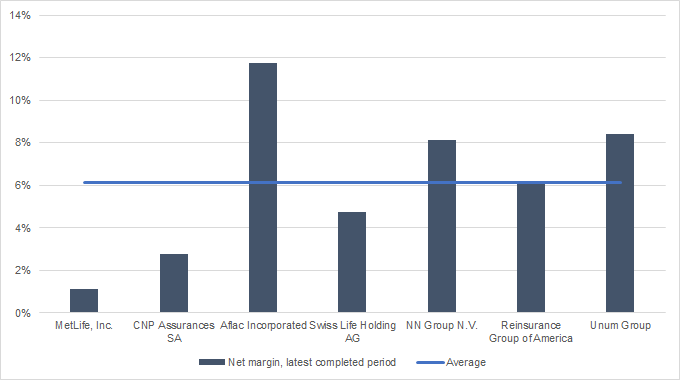

Administrative expenses are mostly related to personnel and office expenses. Whereas most companies provide many types of insurance, we divided companies into two groups: multi-line and life/health insurance. The first group has companies which provide various insurance products, the other group contains companies that mostly focus on life or health insurance.

As for administrative expenses, in multi-line insurance companies, these expenses make up 10% of GWP on average. It is estimated that for Black those costs would be around 5%.

For life and health insurance companies, the result is the same, as administrative expenses make up 12% of gross written premiums.

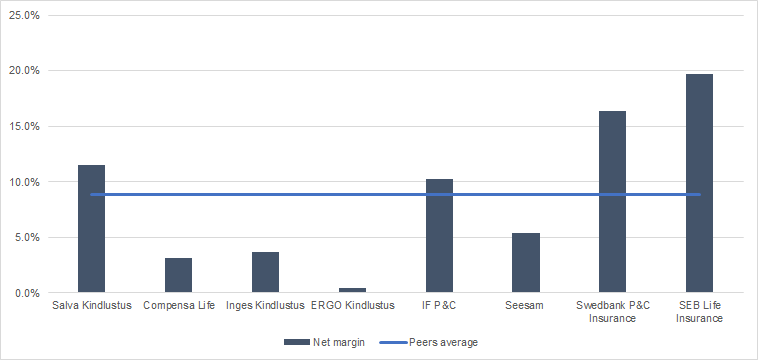

The contrast is quite significant when comparing to the industry’s smaller players. In Estonia, administrative expenses amount to 19% of gross written premiums. Consider that gross written premiums amount to c. EUR 490m in Estonia. That indicates that even small percentages of cost cutting can have an enormous effect on any company.

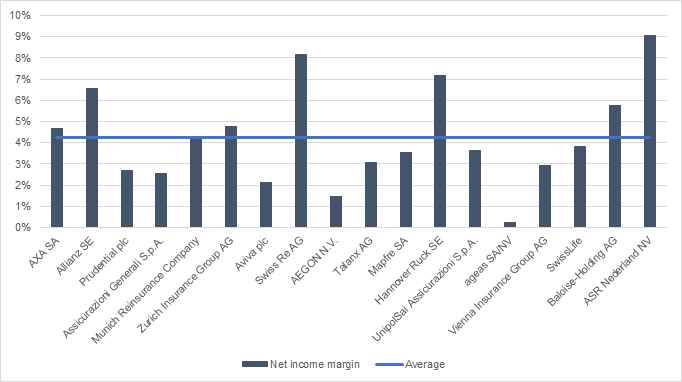

Net margins of the insurance industry’s players

To give a wider picture of the current insurance market, consider the net profit margins of the listed insurance companies. Net margins vary quite significantly between multi-line insurance companies, but none of the peers turned a loss in 2016. The average net margin for the selection of insurance companies is 4.2%.

Margins are slightly higher for insurance companies that focus on life and health insurance, as the net margins for the peers stands at 6.1%.

In Estonia, insurance companies manage to be quite profitable, as the average net margin stands at 8.8% for them. It has to be noted though, that Swedbank and SEB are outliers in this case

Delivering on outcomes is most important determinant of efficacy and effectiveness of educational intervention, irrespective of the scale.

The World Development Report 2018 has put it across very strongly that countries need to prioritise the agenda of learning, and not just schooling, in their policies.

In the past two decades, access and quality issues in educational set-up have dominated discourses in all academic and policy-related forums. All this while, India witnessed many innovations like smart classrooms, app-based learning, online tutoring, and implementation of initiatives like activity-based learning, computer-assisted learning, comprehensive and continuous evaluation, no-detention policy, an initiative of system-wide monitoring through National Achievement Surveys, and above all the Right to Education Act. But a declining trend in learning levels and quality of learning raises the question: “Is providing school education enough?”

Although these initiatives can improve learning, somewhere it implies they could not generate intended return on efforts and investment. The World Development Report 2018 has put it across strongly that countries need to prioritise the agenda of learning, and not just schooling, in their policies. The report reminds policy-makers and stakeholders of education’s promise to learners and public at large.

The pressing challenge

Educational access has failed to keep pace with learning and learning levels. Shortfall in learning is experienced at a very early stage, and builds up as learner progresses through various levels. Studies showed that more than three-fourth learners of Class 2 in rural India could not read a single word in grade-appropriate text (ASER, 2017). About half of students in Class 5 and three-fourth students of Class 8 could read Class 2 level text proficiently. These are not just figures from a study based on a specific sample, they present facts on how India is failing to deliver on the basic promise of education.

The Rashtriya Madhyamik Shiksha Abhiyan launched in March 2009 aimed to increase enrolment rate to 90% at secondary and 75% at higher secondary stage by 2017. It aimed to improve the quality of secondary education by making schools conform to prescribed norms, removing gender, socio-economic and disability barriers, and providing universal access to secondary level education by 2017.

The first goal is very clear. Policy-makers knew how many learners should be enrolled each year to achieve the goal. And we know the results were encouraging. Contrary to this, there is no clearly articulated metric for the quality goal. It sends out an ambiguous signal about the notion of quality and its significance among stakeholders. It is the first and most critical barrier towards meeting quality goals.

Rapid technological changes

It is predicted that most of the jobs that exist today may disappear in the next 10 years. But it is also predicted that there will be demand for different skills in the coming decades. These future skills will require a solid foundation of basic skills and knowledge, which will enable individuals to assess new situations, adapt their thinking and ways of working. This, in turn, will enable individuals to adapt to the economic changes that may occur in their lifetime. It is imperative for systems and countries to build human capital with basic skills, to boost economic growth by facilitating the adoption of technologies and innovations at a faster pace.

Focus on both outcomes & inputs

Most conversations about the education system revolve around increasing inputs, such as textbooks, technology or school infrastructure. The discussion also considers the size of our education system in comparison with other countries, how much it costs the taxpayer to fund the school system, what is the expense of getting a child to complete schooling, how policy has evolved over the years, and so on. However, we tend to pay much less attention to the most important aspect of schooling or education, i.e. its impact on the learners, the knowledge and skills they acquire or need to acquire. School inputs, management and governance should benefit both learner and teacher, facilitate learner-teacher interaction and improve learning. Investments and policies should be driven towards those inputs and processes that can have greatest impact on learners.

Learners & learning outcomes

Delivering on outcomes is the most important determinant of efficacy and effectiveness of any educational intervention irrespective of the scale. The scale may vary from a product or service used at a classroom or school level or a nationwide educational programme or a policy initiative. In this way, education systems can fulfil their promise.

Certain features that make interventions efficacious are:

Learner at the heart: The first challenge is to make all the stakeholders consider for whom are we working, what are the challenges our learners will to face, and what do we need to do to address them. The learning triangle: All the elements of successful learning are available within the classrooms. These elements are the learners with potential and motivation; teachers with the capacity to make an impact on the learner; and the conditions in which teacher and learner interact.

Clear measurable goals: This is the fundamental principle that drives efficacious systems to set clear goals of learning. By defining a target, it is possible to monitor progress towards a goal in real time.

Evidence-based decision: Stakeholders need to utilise the evidence of intended outcomes through valid and reliable measures. They need to understand whether students are achieving targets for the measures defined, how they are performing on skill(s), whether any population groups are lagging and by how much, and which factors are correlated or causally associated with better student achievement.

Monitoring mechanism: A stronger machinery to monitor progress in outcomes, modifying plan of action based on evidence, focusing on areas that are strongly associated with (positively or negatively) learning outcomes are a few factors that improve the possibility of achieving the intended learning outcomes.

The movement has begun?

In the digital age, people’s work and life depend upon their knowledge and skills. In this situation, efficacy measurable impact on learning is quickly emerging as an acid test for the learners, public and decision-makers across many policy areas. This wider trend and movement of commitment and accountability are much needed in India, to which we can contribute, and from which we can learn.

In 2010 in the Us,Department of Education established a national plan “for how technology could provide students with access to engaging digital resources, opportunities to collaborate with peers and experts, and powerful tools to solve real problems as an integral part of the learning experience.” They called it ConnectED and an increase in tablets and Chromebooks began making their way into classrooms.

A year later, higher education collectively embraced Massively Online Open Courses (or MOOCs) as a way to increase enrollment and hopefully reduce rising and increasingly prohibitive tuition costs. But for most classrooms around the country, desks, paper, and pencils still reign supreme. And universities remain rife with PowerPoint lectures and debt-laden tuition.

How, then, should we grade these educational industries? Shirley Malcom of the American Association for the Advancement of Science says it depends on the student, although she seems to favor at least a passing score. “It’s really hard to generalize here,” she says when asked if classrooms haven’t changed significantly since the advent of the Internet. “This is likely true for some but false for others,” she answers while pointing to the successes of flipped classrooms and aforementioned MOOCs.

Where would she like to go from here? If given a magic wand, Malcom says she’d reconstruct the classroom to support more teamwork and smaller group learning. Connected education—analog style, if you will. “Of course I support increased access to and use of technology,” she says. “But I recognize that this is a tool, not the end game.”

And as a key advocate for the advancement of science, technology, engineering, and mathematics, Malcom believes it’s only right to prepare students for an increasingly digital world. Not at the reduction of humanities, mind you. But a focus on those increasingly critical fields.

Minerva Schools in San Francisco is an extreme example of this. No lectures, no labs, no football teams, and no buildings. Everything is done remotely online. Professors have a time limit for talking, and proprietary software tracks which students have spoken in class or not, making participation compulsory.

As for the curriculum, “Teachers will do less teaching and more inspiring,” predicts educator Andrew Mitson in an interview with Synap. “The web will take over straightforward content delivery. Traditional academic subjects will be sidelined for more practical and applicable skills.”

In addition to remote classrooms and more give-and-take between teacher and student discussions, Fast Company reports an unbundling of degrees. "Today, diplomas granted by years in school are the dominant certification of ‘learning.’ Yet, in almost all cases, these diplomas certify nothing other than the fact that the person in question spent x years in school.”

On the other hand, competency-based certifications test specific skills and then bundle those skills into professional groupings for both employers and job seekers.

Take “data scientist,” for example—the most sought-after job in America, according to GlassDoor. As the world record is increasingly digitized, we’ll need an increasing number of researchers to improve computational behavior and understanding. We’ll need even more software developers, especially on mobile. And we’ll need more logisticians, ethical hackers, actuaries Forbes predicts.

What will need to get there and fill all of those jobs and still unseen ones? When dreaming up the future of connected education, we might have over focused on student education and not enough on teacher education, Malcom concludes. “If the above magic wand were really powerful, I’d put a wonderful, smart, and caring teacher in every classroom.”

Tools that enable that, then, might be where the best return on investment exists.

The contents or opinions in this feature are independent and may not necessarily represent the views of Cisco. They are offered in an effort to encourage continuing conversations on a broad range of innovative technology subjects. We welcome your comments and engagement.

We welcome the re-use, republication, and distribution of "The Network" content. Please credit us with the following information: Used with the permission of http://thenetwork.cisco.com/.

The Abdus Salam International Centre for Theoretical Physics (ICTP) is now accepting applications from young physicists and mathematicians for the 2019-2020 class of the Postgraduate Diploma Programme, an intense, pre-PhD programme for talented students. The one year course of study prepares talented students for PhD studies, as part of the Centre’s efforts to promote advanced scientific research in developing countries.

Each successful class of Postgraduate Diploma students helps bring this dream to life. Students have gone on to PhD programmes all over the world, launching them into successful scientific careers. Two semesters of classes are followed by a research project and dissertation.

Study Areas

Interested students can apply to study in one of five subject areas:

High Energy, Cosmology and Astroparticle Physics

Condensed Matter Physics

Earth System Physics

Mathematics

Quantitative Life Sciences

The Quantitative Life Sciences course (QLS) is new this year, aimed at providing students with a quantitative and theoretical background that can allow them to access postgraduate programmes in a broad range of disciplines, including biophysics, quantitative biology, and neuroscience, theoretical systems ecology, economics, data science, and machine learning.

The QLS Diploma Programme will focus in two areas, says Antonio Celani, the QLS Diploma Coordinator. “One will be data science, including statistical learning, artificial intelligence, and machine learning,” Celani explains. “The second area focuses more on biophysics, with courses in neuroscience and ecology and evolution.” The courses are designed to give a core theoretical background for analyzing and modeling different phenomena in life sciences. “But all of these courses for the Diploma Progamme use the language of physics and math.”

Benefits

In each Postgraduate Diploma Programme, scholarships and travel grants will be awarded to those 10 students selected from developing countries. There are no course fees. Students will receive a scholarship of 450 Euro per month for the entire year of study. Accommodation is provided by ICTP.

A limited number of qualified candidates who meet the same selection criteria as others may attend the courses at their own cost. They must supply written evidence from a funding agency or a banking institution that funds are available for their entire year’s stay, and are equal to those offered by the Centre.

SCHOLARSHIP REQUIREMENTS

Eligibility

The Postgraduate Diploma Programme is open to young (generally below 28 years of age), qualified graduates from all countries that are members of the United Nations, UNESCO or IAEA.

The minimum qualification for applicants is a degree equivalent to an MSc (or an exceptionally good BSc) in physics, mathematics or in a field related to the topics listed below. The selection of candidates will be based on their university record and on academic recommendations.

Since the Postgraduate Diploma Programme is in English, fluency in speaking and writing is an essential qualification.

The applicant is expected to have adequate knowledge of the following topics in the specific field for which he/she is applying:

For Condensed Matter Physics: solid state physics; quantum mechanics; statistical mechanics; classical mechanics; electrodynamics; mathematical physics. For High Energy, Cosmology and Astropartical Physics: classical mechanics; electrodynamics; special theory of relativity; quantum mechanics; statistical mechanics. For Earth System Physics: a theoretical background in physics, mathematics or engineering; mathematical methods applied in geophysics and geosciences. For Mathematics: basic abstract algebra; elements of real and complex analysis; topology. For Quantitative Life Sciences: classical mechanics, thermodynamics and statistical mechanics, mathematical methods for physics, basic programming skills

Application

In addition to completing an online application form, candidates should upload the following as part of their application:

Copies of transcripts of university academic records and university degrees in English (The selected candidates will be required to provide originals or certified copies of these documents as well as of their official English translation before he/she can be admitted to the Programme).

Any certificates or documents that give proof of the student’s ability to follow advanced-level courses, study and write scientific literature in the English language.

Two letters of recommendation, from senior scientists familiar with the applicant’s studies and work.

If you have problems with the online application, please contact the Diploma Office at diploma@ictp.it.